Key Takeaways

- Start Early: Start saving for your child's education as soon as possible. Let the compounding of interest do its magic.

- Invest Smartly: Always diversify your investments. It helps balance risk and maximises the returns. There are numerous options available.

- Set Clear Goals: Understand your child's educational aspirations. Create the complete education journey from nursery to university. Then, estimate costs and plan your strategy accordingly.

- Seek Professional Advice: Financial and educational experts, counsellors, and mentors help navigate the long and complex education journey with ease. Benefit from their knowledge, expertise and experience.

Young people between the age group of 18-29 years in India form 22% of the population of the country, a significant proportion of the prospective customers for higher education within and outside India. As more and more people are becoming aware of the importance of education, there is a steep rise in young people whosoever can afford to join colleges and degree courses.

However, this surge in demand has been linked with a sharp rise in educational costs, putting much pressure on the parents. Many families find it hard to cope with such a demand and often make adjustments in the quality of education. The good news is, such a situation can be avoided through proper planning. Here are some important tips on how to ensure you, as a parent, save for education effectively and your children get the education they deserve:

Start Early: The Advantage of Compounding

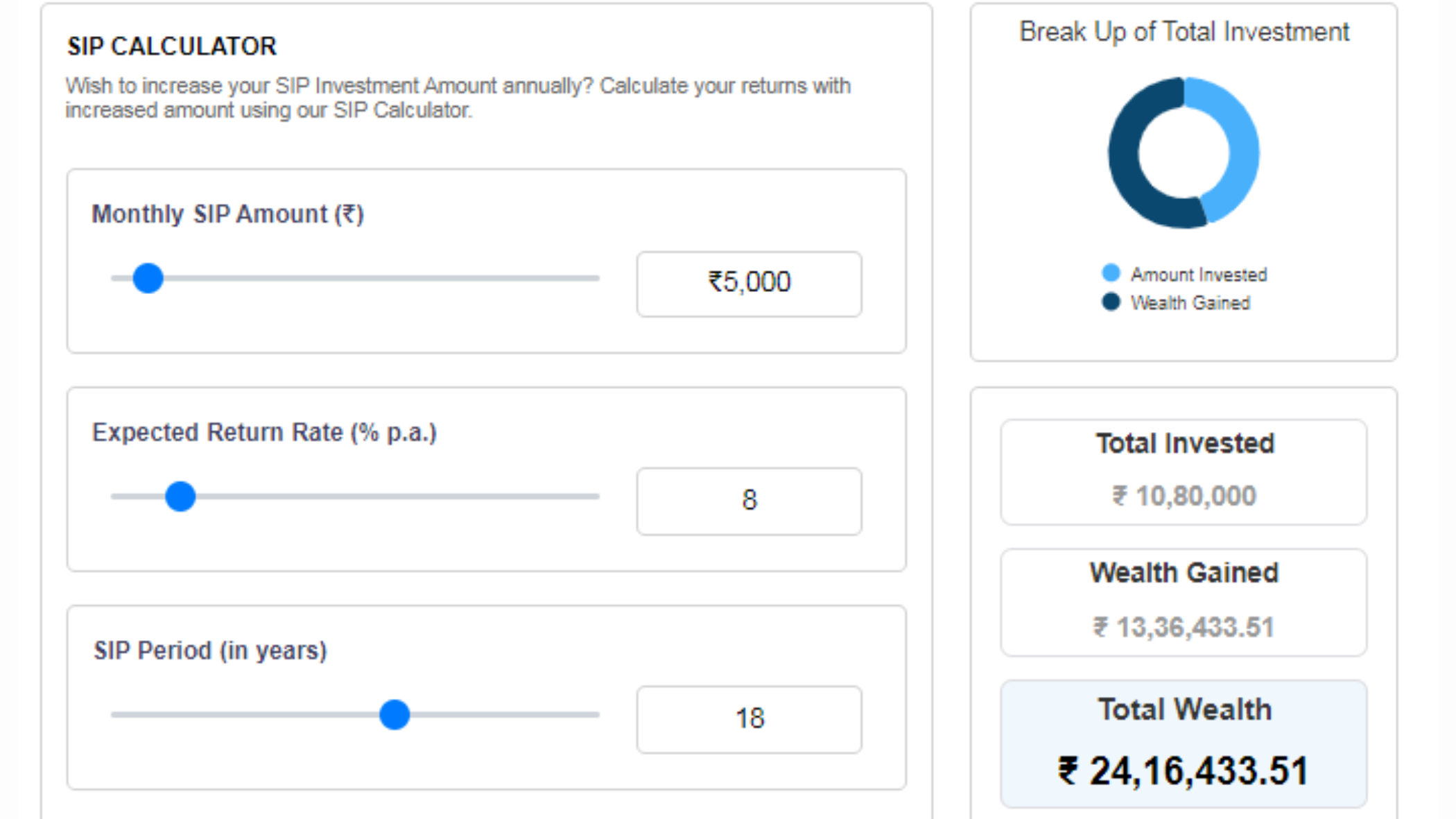

As they say, "The early bird catches the worm." This adage applies to financial planning, too. An early start in saving for your children's education makes all the difference. Providing for their child's future always is the top priority of parents. The early start gives time for your savings to grow over time, using compound interest effectively. For instance, if you invest Rupees 5,000 every month from your child's birth, at an average return of 8% per annum, you would have built a corpus of more than Rupees 24 lakh when your child reaches the age of 18. This will form a considerable sum for their higher education.

Invest Smartly: There are Many Investment Options

Do not put all eggs in one basket. Starting early must be supported by smart investment strategies. Diversification, for one, reduces risks and maximises returns on your investments. You can consider investing in a mix of fixed deposits, mutual funds, PPF, and other products. Especially equity-linked savings schemes and mutual funds can deliver higher returns in the long run. Through a systematic investment plan (SIP), you can invest a constant sum in mutual funds at regular intervals. This helps you take full advantage of rupee cost averaging and compounding.

Set Clear Goals: Planning the Education Journey for a Better Outcome

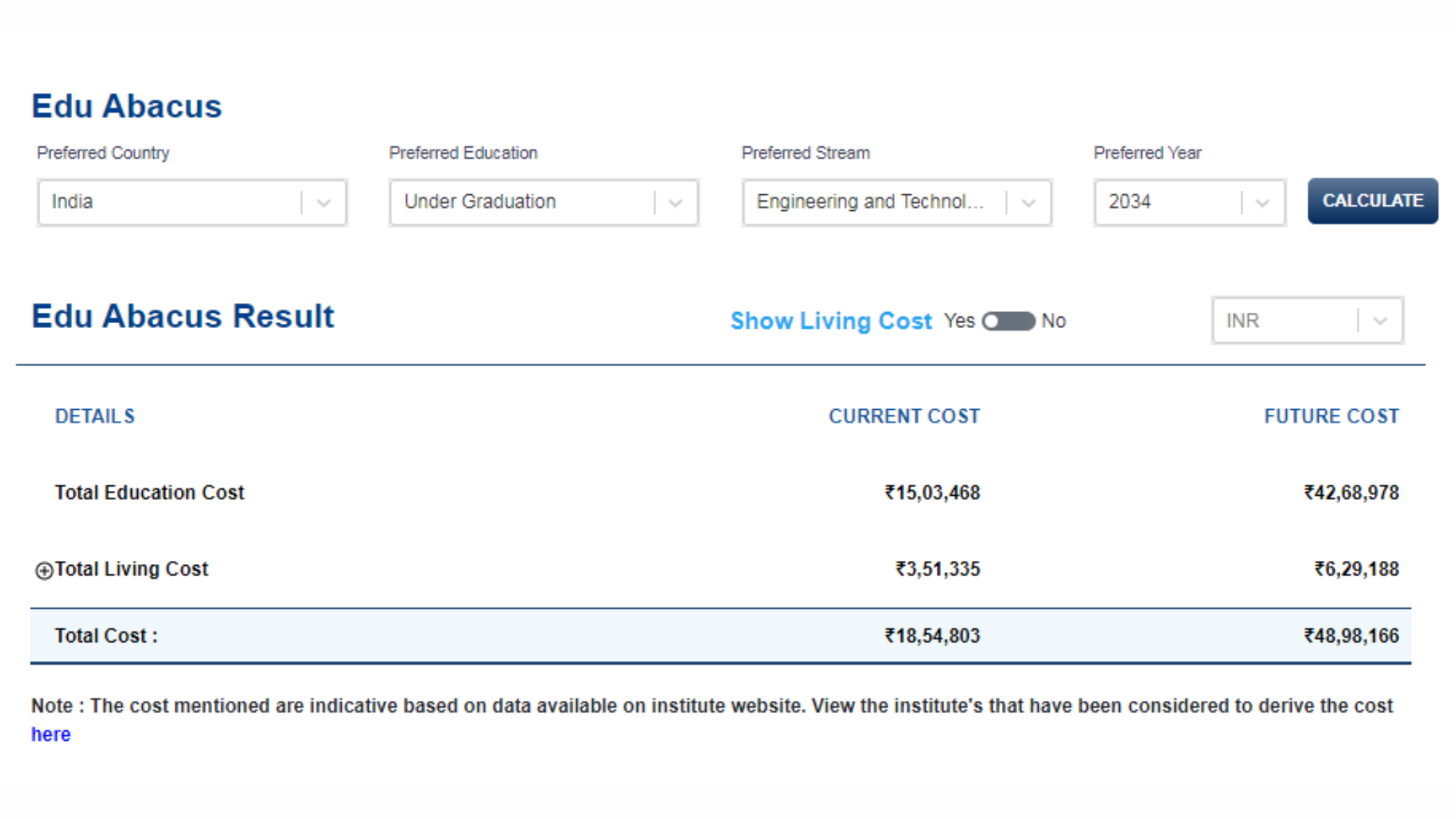

Knowing what aspirations your child has regarding his or her education helps in formulating your saving strategy. Is your child interested in engineering, medicine, or arts? Do they want to study abroad? What will be the cost of education in the future, at the time they go to college? Knowing these details helps in estimating the funds that are required. For instance, 10 years from now, doing an engineering course in India is likely to cost around Rupees 49 lakh while the current cost for the same course is only around Rupees 18 lakh. Setting clear goals will help you estimate how much you need to save every month to achieve that target. It also helps with dedicated savings and consistency.

Plan for Achievable Goals: Savings vs. Income

Your money-saving scheme should align with your financial reality. Make an estimate of your monthly income and expense levels, and work out the best amount that you can save every month. Over-ambitious targets without robust planning may lead to financial distress. For example, if you think Rupees 10,000 per month is a reasonable amount you can save, ensure that this amount does not affect your other life goals, savings for health, and emergency backups.

Talk to Experts: They Know How to Help

Devising an overarching strategy for education planning is challenging. Understanding financial products and investment options can be overwhelming. Professional advice can help shed light on all this and offer solutions. A financial planner, education expert, counsellor, or dedicated organisation, such as Invest4Edu, can offer advice based on your individual needs and help you select the best possible investment strategy. They can also help you with career counselling, estimating costs, and comparing various financing options. With their expertise, the process becomes easier and clearer, guaranteeing that you make the right decisions, which coincide with your child's potential.

Planning for the higher education needs of your child requires proactivity and precise information. The earlier you start with smart investments, clear goals, and professional advice, the better you will be equipped to fulfil your children's educational requirements.